Real Estate Term of the Day: Government National Mortgage Association (Ginnie Mae or GNMA)

GOVERNMENT NATIONAL MORTGAGE ASSOCIATION (Ginnie Mae or GNMA) – a government organization to assist in housing finance. Nicknamed Ginnie Mae, there are two main programs: 1) to guarantee payments to investors in mortgage-backed securities and 2) to absorb the write-down of low-interest rate loans that are used to finance low-income housing (Barron’s Dictionary of Real Estate Terms)

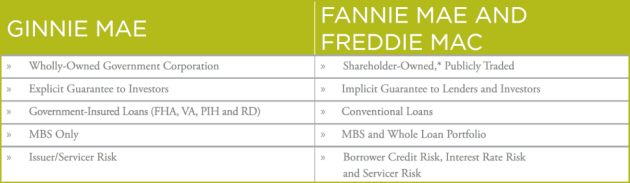

Below is an explanation of the key differences between Ginnie Mae and the Government-Sponsored Enterprises (GSEs), Fannie Mae and Freddie Mac (source: ginniemae.gov):

-

Only Ginnie Mae securities are explicitly backed by the full faith and credit of the U.S. Government. Ginnie Mae, Fannie Mae, and Freddie Mac guarantee mortgage-backed securities (MBS) for timely payment of principal and interest.

-

Ginnie Mae is a self-sustaining, profitable and wholly-owned government corporation located within the U.S. Department of Housing and Urban Development (HUD), while the GSEs are public corporations chartered by Congress, but owned by shareholders*. As a wholly-owned government corporation, Ginnie Mae is not required to make decisions to increase value for shareholders; rather, it can remain soley focused on its mission of providing support for affordable housing.

-

Ginnie Mae’s conservative and stable business model significantly mitigates taxpayers’ exposure to risk associated with mortgage securitization. Unlike the GSEs, Ginnie Mae acts only as the guarantor on the pools of federally-insured or guaranteed loans. Fannie Mae and Freddie Mac, however, guarantee the loans themselves. Another differentiating factor is that Ginnie Mae does not purchase mortgage loans for generating profit, nor does it actively buy, sell, or hold securities for investment purposes. Rather, approved private lending institutions issue the MBS for which Ginnie Mae provides the guaranty.

-

In the Ginnie Mae program, Issuers are financially responsible for their securities, even if the underlying mortgage collateral becomes delinquent. While the GSEs are responsible for the financial losses related to the loans in their investment portfolios and MBS, the Ginnie Mae Issuer must make principal and interest pass-through payments to investors for delinquent loans, as well as provide the funds to re-purchase loans to foreclose on a home or modify a loan. Ginnie Mae Issuers are responsible for any unreimbursed costs associated with either violating insurers’ servicing guidelines or for inadequate insurance coverage. This requirement provides a strong incentive for private institutions to make better quality mortgage loans. It is important to note that Ginnie Mae does not have a financial obligation to MBS investors unless the Issuer becomes insolvent.